Ever since our re-emergence from the pandemic years, our need for security and wealth is stronger than ever and owning a house is a safe way to achieve this. Unfortunately, soaring housing prices in Malaysia are still driving people away from the dream.

While you can always apply for a housing loan to purchase your first home, there are alternative sources you could opt for, some of which may come as a surprise for you: your EPF!

While the Employees’ Provident Fund (EPF) is designed to support your life post-retirement, few of us know that it could be used to purchase your next home in more ways than one!

| 1. Where & How To Start 2. What You Need 3. How Much You Can Withdraw 4. How To Apply For Withdrawal |

1. Where & How To Start

First and foremost, let’s get the basics out of the way.

The amount that is found in your EPF is the sum of monthly deductions from your income. The percentage of its deduction typically ranges from 9% to 11% (11% being the mandatory rate for employees). You will only be able make withdrawals from your EPF after age 60. Simple enough right?

Your EPF account is comprised of two accounts: Account 1 & Account 2.

Account 1

Your retirement savings only go to Account 1.

Of the total sum of your monthly salary that gets allocated to your EPF, 70% of that total sum is allocated to Account 1. The remaining 30% will go to Account 2; we’ll get to this later!

Account 2

This is where the magic happens. 30% of the total sum that gets allocated to your EPF every month goes to Account 2, whereas the understandably larger 70% share is reserved for your retirement savings in Account 1.

Unlike Account 1, you can make withdrawals from Account 2 before age 60 but only for specific financing purposes, most prominent of them being the ability to finance a house purchase(s). You may also make joint withdrawals with your spouse and other familial relations for this purpose.

“Can I Withdraw My EPF to Pay House Loan?”

Yes! You can make withdrawals to reduce/redeem housing loan balance for a house. You can also assist your spouse to reduce/redeem housing loan balance.

Besides home financing, your Account 2 can be withdrawn to pay off medical expenses and finance you or your children’s education as well. As for our Muslim brothers and sisters, your Hajj or pilgrimage can be financed with Account 2 in tandem with your savings from Lembaga Tabung Haji (LTH). Read more here for the full list!

2. What You Need Before Withdrawing

Prior to financing your first housing purchase with Account 2, you must first produce these documents to ensure a smooth application process:

1. Produce Form KWSP 9C (AHL)Alongside a copy of your MyKad & bank account statement (passbook also accepted). |

2. Sales and Purchase Agreement (SPA)SPA must be within 3 years since date of application. |

3. Proof of Financing – *Additional Document for Bank Loans*You are required to produce your Housing Loan Approval Letter received from your lender as proof of your legitimacy. If exceeded 1 year since date of housing loan approval, produce additional proof of (any 1 of):

|

4. Proof of Relationship – *Additional Document for Bank Loans**Compulsory for joint withdrawals with spouse, children, parents, etc. Produce marriage certificate or birth certificate. |

3. How Much You Can Withdraw

The amount that you can withdraw from Account 2 will differ based on how you choose to finance your housing purchase, typically to apply for bank housing loan or via self-finance.

Via Bank Housing Loan

There are two methods that are simultaneously taken into consideration:

- Difference between purchase price and approved housing loan amount + 10% of the purchase priceOR

- All savings in Account 2

The amount in which you are able to withdraw will be whichever is lower between the two.

Via Self-Finance

Similar to bank housing loan, there are two methods that are simultaneously taken into consideration:

- The purchase price + 10% of the purchase priceOR

- All savings in Account 2

Whichever is lower between the two will be the amount that you are able to withdraw.

For joint withdrawals, the same methods apply except that your partner’s entire savings in Account 2 are also included in the calculation.

4. How To Apply For Withdrawal

Now that you’ve learnt more about EPF’s open secret, you can begin to know how to withdraw from Account 2 to purchase your dream first home! KWSP have thankfully streamlined the application process to online — so you can skip their infamously long queues at their physical locations!

However, you must first register with KWSP as an i-Akaun member prior to the application process. For registration, you must register at a nearby KWSP counter or kiosks but worry not, their friendly attendants will guide you through the process which is especially helpful if you are not tech savvy.

After you’ve registered, head on to KWSP’s official website and log in to your account using your your i-Akaun credentials and follow these simple steps:

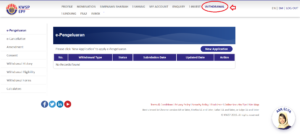

Step 1

Once you’ve logged in, you will have to click on the “Withdrawal” tab (as highlighted below) on the top menu bar.

Once you are there, you will find records of your withdrawals (if any) neatly outlined along with its status, withdrawal type, and submission and updated date for your convenient perusal.

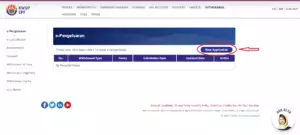

Step 2

Click on “New Application”

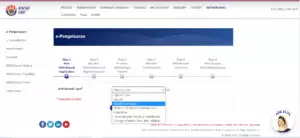

Step 3

Once you are directed to the new page below, click the “Withdrawal Type” drop-down menu and choose the “Buy/Build House” option.

You can also choose to apply for the option to reduce/redeem your housing loan here.

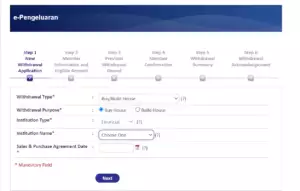

Step 4

Pay extra attention to this step, or rather, a series of mini-steps. You will have to choose the option between “Buy House” or “Build a House” (in this case, choose the “Buy House” option).

Next, choose your lender (i.e. your bank) from “Institution Name” drop-down menu. However, do note that only 4 banks (CIMB Bank, Maybank, Affin Bank, RHB) are listed on the drop-down menu so it is recommended that you open an account with any of the said banks and apply for a housing loan there ahead of time.

Last but not least, be sure to accurately input your Sales & Purchase Agreement date and the rest should be straightforward enough!

If for whatever reason your withdrawal application is deemed ineligible, you will be taken to the page below. Should this happen, redo the application in case there were any mistakes on your part. If that fails, check if you’ve fulfilled these prerequisites:

- Must have a minimum RM500 balance in your Account 2.

- Must be below the age of 55.

- Must be less than 3 years since the signing of your Sales and Purchase Agreement (SPA).

- Check your housing loan status with your bank – your loan must be approved first!

And there you have it! Who knew you could draw from your retirement savings to purchase a house, right?

While the “EPF Account 2 withdrawal for house method” is admittedly not the most surefire way of purchasing a house, it is sufficient enough to reduce the effects of rising cost of living, and soaring housing prices by dampening the price of the house.

Looking to learn the ins and outs of real estate? We at Juwai IQI are here to help you hone your skills. Join us today!

[hubspot type=form portal=5699703 id=c063034a-f66d-41ab-881b-6e6a3f275c33]